The bottom line of any grant application is the foreseen budget and the requested grant amount for the project. In this regard, Horizon Europe is no exception. Grant application reviewers will typically refer to the budget to discern additional information about the overall quality of the proposal and to realize the work plan’s strength or, otherwise, discover potential flaws. Moreover, the reviewers will have to assess whether the project implementation structure and the allocated resources are appropriate and justified to achieve the project’s goals. Therefore, the presented budget must correlate with the expected efforts and tasks detailed in the work packages and reflect the quality of the overall work plan. For this exact reason, we have created this useful guide for preparing the Horizon Europe project budget. We will begin with a technical overview of the Horizon Europe proposal in terms of the budget sections and then continue with our recommendations for how to best construct the budget for your project.

A technical overview of the Horizon Europe budget sections

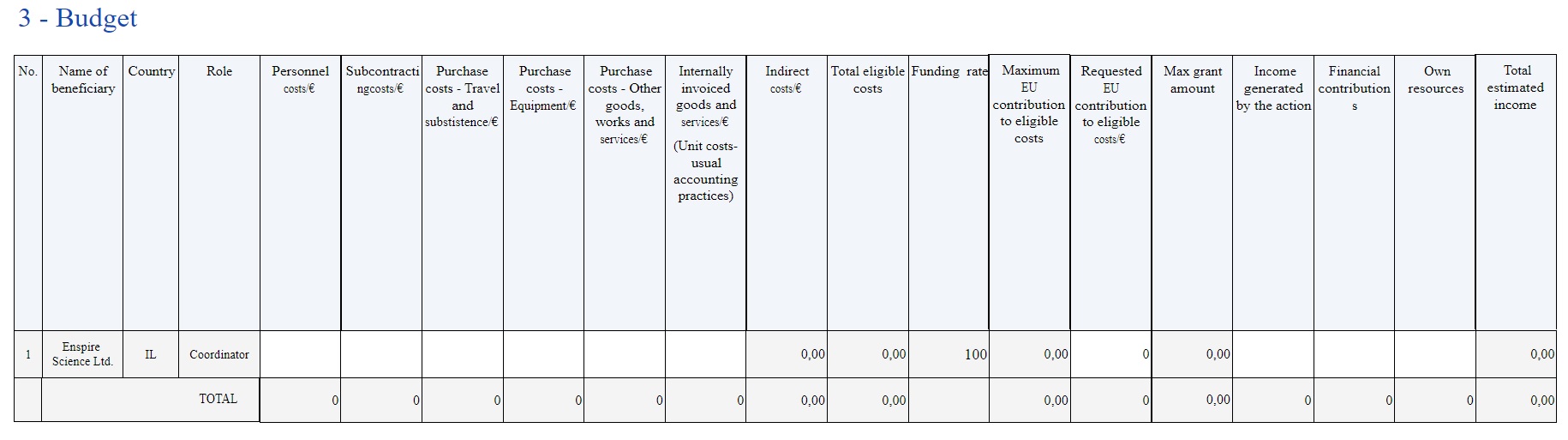

The budget of the Horizon Europe project is presented both in Part A and Part B of the Horizon Europe proposal. The budget table in Part A presents the ‘bottom lines’ for each partner, and the total for the entire project. It includes all the project’s direct costs and the additional 25% flat rate of indirect costs (only for the entitled direct costs). The expected grant for a specific project is indicated in the information provided in the topic description. The budget presentation in Part B is more elaborated. Let’s quickly review these below.

Budget presentation in Part A:

The budget table in Part A (in the electronic forms) presents only the budget’s “bottom line” figures for each partner for the entire project duration, using a breakdown of the defined cost categories, as reflected in the image below (click the image to enlarge).

Budget presentation in Part B:

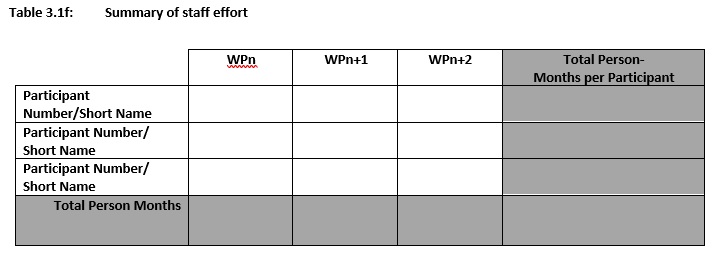

The budget of the project is more elaborately presented in Part B section 3.1. It starts with the detailed information provided in the “Description of work” in each of the work packages (Table 3.1b). The information in these work packages serves as the main justification text for the budget request. Then this is complemented by the information provided in the following four different tables:

Table 3.1f – A Summary of staff effort – the information about person-month allocations per partner and per work package should be summarized under this table (should perfectly reflect and summarize the information provided in the various work packages).

Table 3.1g – A table showing a description and justification of subcontracting costs for each participant – Each partner should describe the tasks that it is going to subcontract (if any) and proper justification for that, alongside the associated costs.

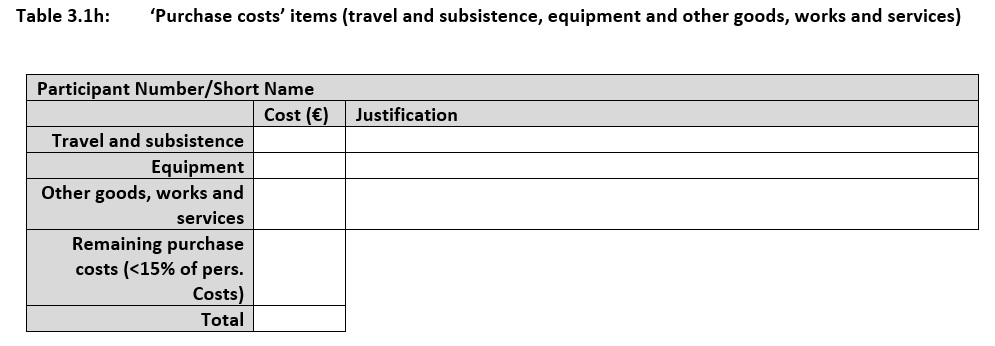

Table 3.1h – A list of ‘Purchase costs’– Information and justification for purchase costs of the following cost categories (per partner): travel and subsistence, equipment and/or other goods, work and services. The rule here is that each partner should provide details for the purchase costs that sum up over 15% of the personnel costs allocated to the partner. The sum of the remaining purchase costs that are below the 15% mark (of personnel costs) can be presented here without additional justifications.

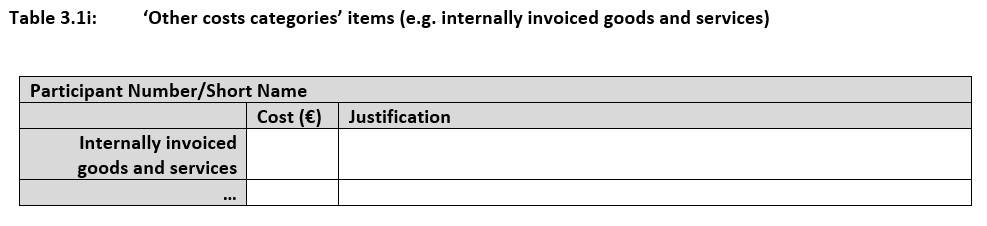

Table 3.1i – A list of ‘Other costs categories’ – There are several ‘other costs categories’, in addition to the ones mentioned above, that can be added to the Horizon Europe project’s budget. If one of these other cost categories is relevant to your project, a justification under table 3.1i should be provided. Keep in mind that most of these ‘other costs categories’ cannot benefit from the addition of the 25% flat rate of indirect costs.

Having understood the basic requirements for each budget table in both Part A and Part B of the Horizon Europe proposal, the next step is a more conceptual discussion regarding how to construct a strong budget that accurately reflects the project’s concept and objectives, and successfully “feeds the reviewers”. Continue reading below.