Planning the budget for your project can be one of the most complex aspects when applying for different grants under Horizon Europe. Fortunately, this is not the case for the MSCA Doctoral Networks (DN) and MSCA Postdoctoral Fellowships (PF) grants (as well as other Marie Skłodowska-Curie Actions), in which the budget is based on fixed unit contributions and is automatically calculated for the applicants based on specific conditions such as the country in which the fellowship will take place, their family status, and so on. While there’s not much latitude in the budget planning at the proposal stage, it is still essential to get familiarized with the different budget categories and their specifics in order to fully understand how the financial aspects of the project should be managed. To this aim, we’ve written this MSCA DN/PF budget guide that will walk you through the various categories and specifications.

The structure of MSCA DN and MSCA PF budget

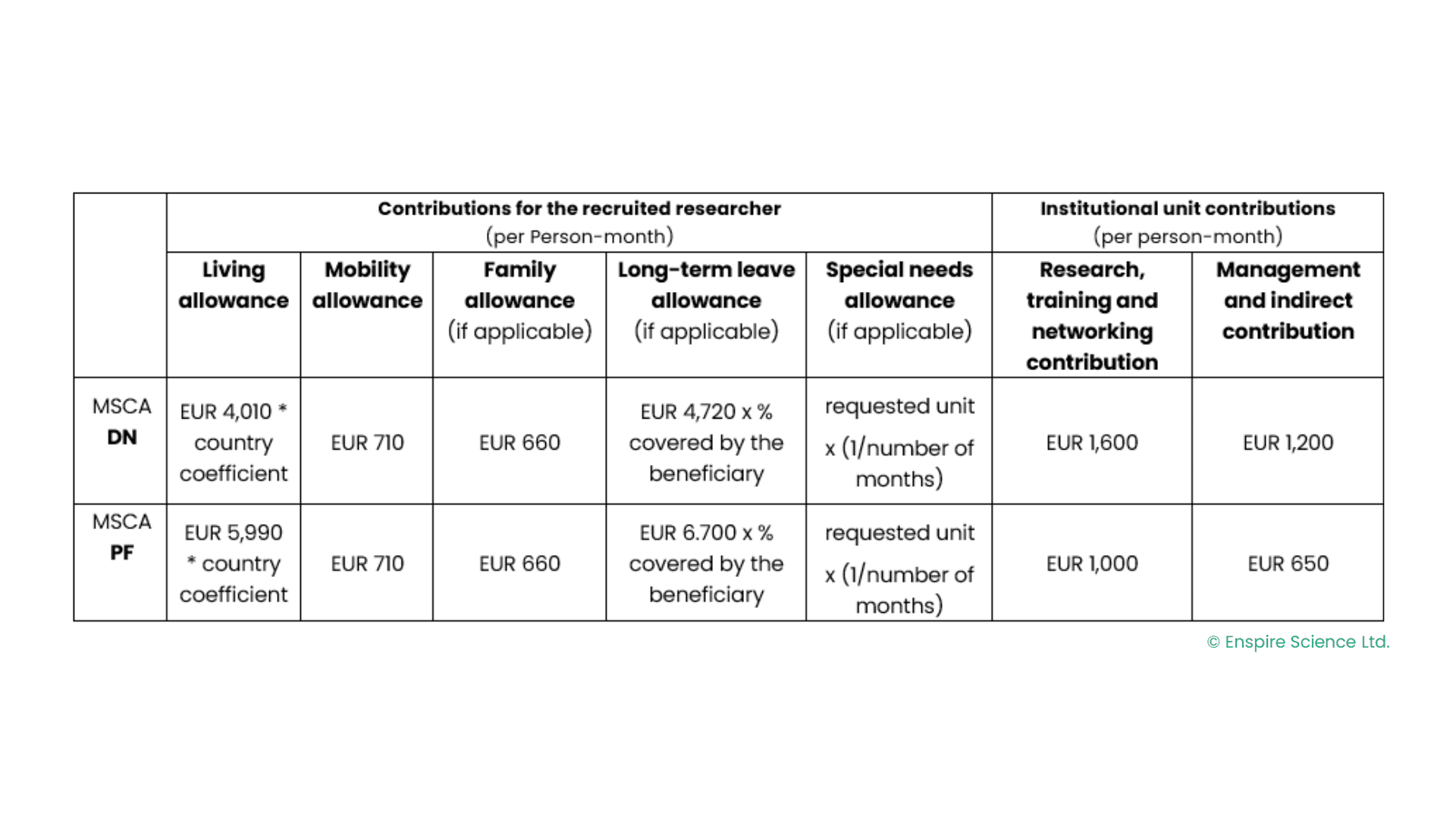

The MSCA DN and MSCA PF budget is structured according to a fixed monthly unit contribution for the recruited researcher and a fixed monthly institutional unit contribution. Each of these two budget categories are divided into several categories, as shown in the table below.

Let’s look closer at these two budget categories and their respective sub-categories:

- Contributions for recruited researchers – This budget category refers to the budget allocated for the employment costs and other costs paid to the recruited researchers – Doctoral Candidates (DCs) in the case of DN, and post-doctoral candidates in the case of PF. The EU contribution for the researcher is transferred to the beneficiary. The beneficiary recruits the researcher under an employment contract and pays them all costs which are directed at the researcher’s living and well-being, as follows:

- Living allowance – The living allowance covers the beneficiary’s cost of employment and is aimed to provide the researcher with financial security throughout the project. To ensure equality for all recruited researchers, and account for the different costs of living in different countries, the living allowance is adjusted according to a country coefficient, depending on the country where the recruiting beneficiary is located. The country correction coefficient list can be found at the end of the MSCA Work Programme. The living allowance is a gross amount, which means that all compulsory social security contributions, direct taxes, and any other compulsory deductions under national legislation are deducted from this gross amount. The recruiting beneficiary may choose to add extra payment on top of the grant contribution.

- Mobility allowance – The mobility allowance is aimed at covering private mobility-related costs of the recruited researcher, including travel and accommodation costs. This contribution does not cover travel for professional or research purposes.

- Family allowance – A fixed family allowance is provided for married researchers, as well as for researches with a status equivalent to marriage recognized by the country in which the relationships were formalized. Researchers with dependent children are also eligible for receiving family allowance. Should the fellow’s personal status (marriage, children) change during the action, they will become eligible for family allowance as well.

- Long-term leave allowance – The long-term leave allowance covers the costs of a researcher’s leave for a long period due to personal circumstances, such as maternity or paternity leave, long sick leave, or other special leaves longer than thirty consecutive days. The contribution will be provided against a reported need.

- Special needs allowance – The special needs allowance is provided for researchers with disabilities, whose long-term physical, mental, intellectual, or sensory impairments are certified by a national authority. The allowance covers costs related to the fellow’s disability which are necessary for participation in the action. The special needs allowance will be provided against a reported need.

- Institutional unit contributions – This budget category refers to the budget allocated for the costs of the work performed in the project and its execution. The following sub-categories are included in this category:

- Research, training and networking contribution – This contribution covers the costs of the project activities related to the research work and the various training and networking events and activities. This includes:

- Career development activities such as conference participation, publication costs, hard and transferable/soft-skills courses, requiring registration fees and/or travel costs.

- Research expenses such as consumables, or the use of facilities or infrastructures.

- Visa-related fees and travel expenses

- Additional costs for travel and accommodation arising from secondments which require physical mobility.

- Management and indirect contribution – This contribution covers the costs related to project management and additional institutional costs related to the project, such as indirect costs or personnel costs for the project’s management and coordination.

- Research, training and networking contribution – This contribution covers the costs of the project activities related to the research work and the various training and networking events and activities. This includes:

MSCA DN budget specifications

While MSCA DN and MSCA PF budgets are quite similar, there are some specifications that apply to the MSCA DN funding scheme in particular.

First, all DN projects must comply with the 40% rule stating that no more than 40% of the total budget can be allocated to beneficiaries from the same country or to a single International European Research Organization or International Organization. Proposals not complying with this rule will be counted as ineligible.

Another unique aspect of the MSCA-DN budget is that the consortium may decide to redistribute the institutional unit contributions (the research, training and networking and management and indirect contributions). For example, the consortium may decide that since the coordinator is planned to incur higher costs related to management of the action, all beneficiaries will allocate some of their institutional unit contributions to the coordinator. Alternatively, if one of the beneficiaries (or associated partners for that matter) is planned to hold a training/networking event with substantial costs, the consortium may decide how to allocate funds to cover the costs of this event. It is recommended that any such redistribution is agreed upon beforehand and included in the Consortium Agreement.

With respect to MSCA DN Industrial Doctorates (ID/ Joint Doctorates (JD), while not mandatory, multiple consecutive recruitments should be taken into account. Since the living allowance is affected by the country correction coefficient, the recruitment periods in the different beneficiary organizations should be well-planned. Let’s take as an example an MSCA DN-JD fellowship of 36 months, in which the fellow is recruited by a German university, but a minimum of 12 months should be spent in the location of a Danish university in order to obtain a joint/double degree from both universities. The country correction coefficient for Germany is 98.3% (of the fixed amount of the living allowance) while in Denmark it is 132%. In this case, recruiting the fellow for 36 months in the German university with a stay (e.g., as a secondment) of 12 months in the Danish university will have a negative effect on the fellow’s ability to afford the cost of living, as the living allowance will be calculated according to the coefficient of Germany, while the living expenses in Denmark are higher. Offering the fellow a contract of 24 months in the German university and a contract of 12 months in the Danish university will guarantee that they have the capacity to afford the living in each location.

Conclusion

As can be seen, there are various considerations to keep in mind when structuring the budget plan for either MSCA PF or MSCA DN projects. As you work on your research proposal for these funding schemes, be sure to keep this article close by! For any specific questions and advice, follow this link to learn more about how we can guide your upcoming MSCA PF or MSCA DN proposal application.